Chart of accounts

A chart of accounts specifies the rules for preparing a company’s financial statement. It is an important tool for organizing and classifying financial data and ensuring that a company’s financial statement is prepared systematically and correctly. A chart of accounts defines the accounts that are used in financial statements and specifies how these accounts should be named and numbered.

The chart of accounts generally consists of three main parts (in MonetShark this is managed through the Account type field):

- Balance Sheet Accounts: This section refers to the accounts that represent the company’s assets, equity and liabilities. These include accounts that record the company’s assets, such as buildings or cash, inventory, debts, and accounts payable.

- Profit and loss accounts: This part indicates the accounts in which the company’s income and expenses are recorded. This includes accounts that record sales, revenue from services, and company expenses for purchasing services.

- Off-balance sheet accounts: This section includes all other accounts that are not directly related to balance sheet accounts or profit and loss accounts and do not directly “participate” in the preparation of financial statements.

The chart of accounts may vary depending on country legislation and company specifics. It helps ensure that financial statements are drawn up consistently, which is important not only for the company’s internal management, but also for its external financial reporting purposes, such as meeting the requirements of the tax inspectorate or presenting to investors.

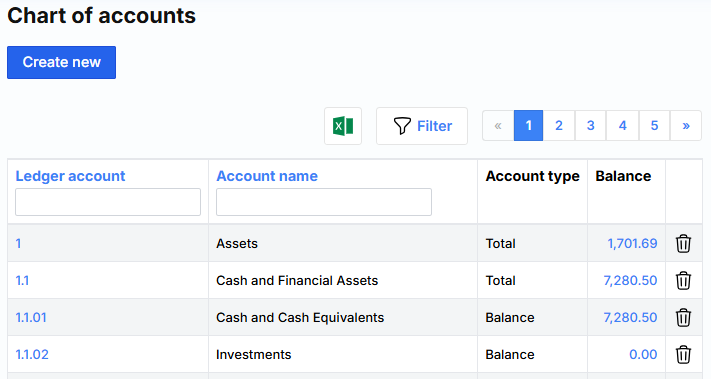

The list of MonetShark accounts looks like this:

Ledger account – DK account code, which must be unique.

Account name – DK account description.

Account type – indicates the type of account. The three most commonly used are Balance , Gain and Range , and Total . The type determines how the Letger account amounts will be treated at year-end closing. Balance , Assets , Debts – the balance is carried over to the next year. Profit and Range , Income , Expenses – closes through 3rd class.

Balance – shows the total amount of that account or, if it is aggregated by a DK account, of that group of DK accounts over the entire period.